On the topic of marking to market…

I’ve talked about the private equity and in particular private credit bubble, and how multiple PE funds have gated investors. Now we see the dolts running Harvard’s money are neck deep in this garbage. Not surprised, really.

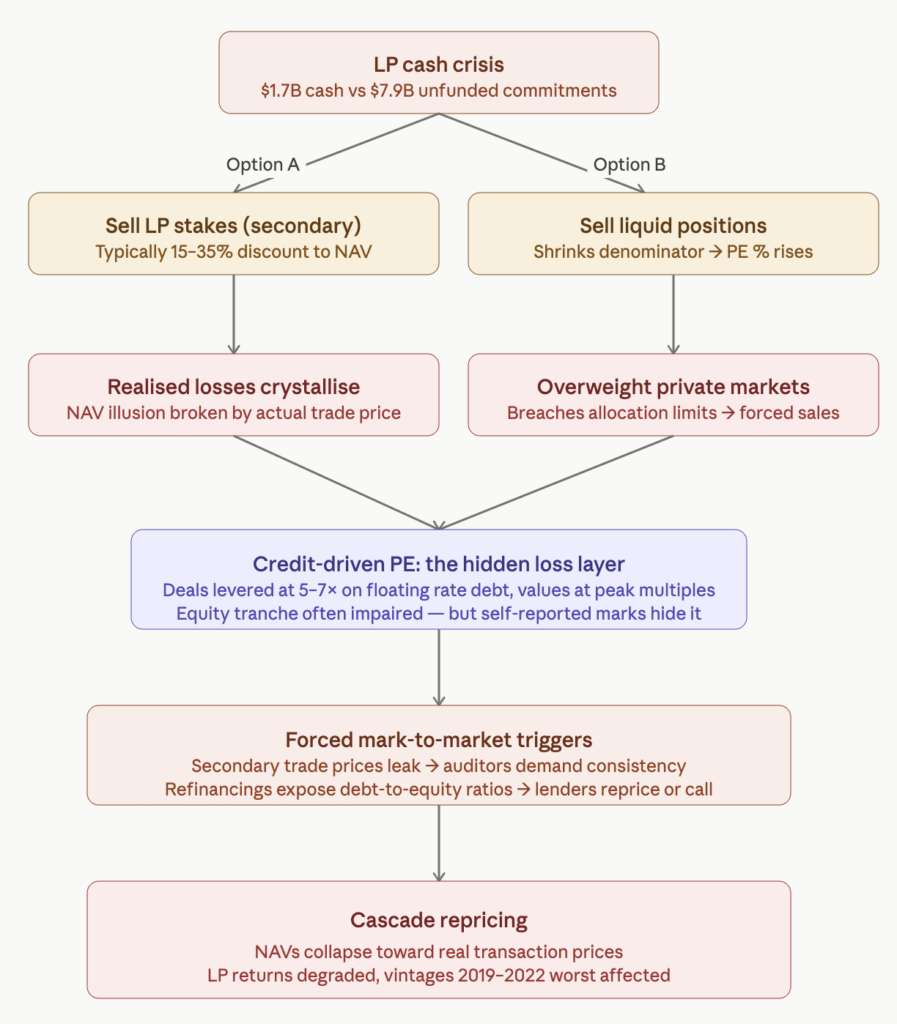

The liquidity trap the poor suckers at Harvard (spineless pointy shoes) are facing is ultimately a forced mark-to-market event in slow motion.

Private equity funds have been able to paper over deteriorating portfolio valuations because the exit environment has been essentially closed. No IPOs, no strategics buying at 2021 multiples, no secondaries at par. As long as nothing trades, nothing prices. But the denominator problem now forces action, and once you start selling — whether LP stakes or liquid positions — you shatter the fiction.

The credit piece is the real kicker…

A massive proportion of PE deals done in 2020–2022 were levered on floating-rate debt against assets valued at peak multiples. Rate normalisation compressed the equity cushion from both sides: with rates rising, the cost of capital went up, EBITDA multiples came down.

The equity is often deeply underwater in economic reality, but GAAP fair value accounting for PE portfolios is self-reported — they mark to comparable public multiples with a liquidity discount applied at the manager’s discretion. That discretion has been used liberally.

The cascade looks like this:

The key mechanism that makes this inevitable rather than merely possible:

Self-reported marks can’t survive transaction evidence. Every time a secondary trade clears — even one — it creates a pricing reference that auditors and limited partners can point to. If a fund’s NAV says 1.0x and a secondary buyer just paid 0.65x for a stake in the same portfolio, the discretion evaporates. Auditors increasingly require consistency across observable transactions.

Debt refinancing is the real execution wall. The deals that got done at 6–7x leverage in 2020–2022 used term loans that eventually mature. When a PE-owned company comes to refinance in 2025–2027, it’s doing so at 200–300bps higher rates, against an EBITDA that may have flatlined, and into a lending market that is repricing credit risk.

The lender’s valuation process will mechanically surface what the equity is actually worth — often zero or close to it on highly levered deals. That’s not a discretionary mark. It’s a covenant breach or a renegotiation that becomes public.

This is why you’re seeing PE funds gating redemptions.

The denominator effect tightens the noose. Selling liquid equities to meet capital calls or operational needs shrinks the total portfolio, making private markets a larger percentage by mechanical math — even if the underlying PE valuations haven’t moved. This creates regulatory and mandate pressure at pension funds and endowments to reduce PE exposure, which feeds more secondary supply, which feeds more price discovery, which feeds more accurate marks. It’s self-reinforcing.

The historical analogue is 2008–2009, where PE NAVs were slow to move, then moved violently when refinancing cycles hit and bank lenders stopped extending. The difference this time is the sheer scale — 41% private market allocations across major institutional capital bases is a systemic concentration, not a niche problem.

Between private equity, private credit, and the AI bubble, the odds of things chugging along peacefully without any violent speed bumps seem like a slim probability. Rather, I think a concrete barrier is going to be hit.

Editor’s Note: Private equity’s coming reckoning is only one part of a much larger picture.

Sky-high debt, reckless money printing, political instability, and deep social changes are all converging at once. That means the years ahead could bring extraordinary volatility—not just in markets, but in everyday life.

That is why we’ve put together a free special report that explains the major economic, political, and cultural trends unfolding right now, what they could mean for your money and personal freedom, and how a contrarian investor is thinking about staying one step ahead.

You can get the full report here.

Read the full article here